- por Sheldon Kimber, CEO, cruzar o poder

O clima está aquecendo e nossa sociedade será forçada a descarbonizar além do setor de potência. Isso é certo, e apenas uma questão de tempo. Ao mesmo tempo, a eletricidade limpa está atingindo níveis sem precedentes de acessibilidade e disponibilidade, e nem tudo isso pode ou deve encontrar o caminho para a rede elétrica. Acredito que a combinação desses dois fatores resultará em crescimento exponencial em cinco indústrias inevitáveis que têm o potencial de obter o planeta para obter zero emissões por conta própria, sem novos avanços maciços.

Eu tenho discutido isso nos últimos anos, mas finalmente cheguei a escrevê -lo. O que se segue é uma tese de cinco partes que cobre uma visão potencial de nosso futuro de baixo carbono, uma visão geral da dinâmica importante que dita a direção dessa transição e alguma discussão sobre quem pode se beneficiar e como.

Outros podem ter escrito sobre peças distintas dessa visão abrangente, mas acho que a Intersect tem uma visão exclusiva e ousada, combinada com uma equipe que sabe o que é preciso para construir infraestrutura física nessa escala. Minha esperança é que você ache isso tão inspirador e esperançoso quanto eu. Espero que deixe você otimista de que, de fato, exista um caminho para resolver a crise climática com tecnologias bem compreendidas sendo implantadas em uma escala muito maior em diferentes áreas da economia do que antes. Esta é a visão que me faz entrar no trabalho todos os dias e me permite dizer aos meus filhos que há um caminho a seguir para a geração deles.

Parte um: Os planos de negócios são fáceis quando você conhece o futuro

Tenho várias perguntas básicas, mas úteis, que usei para enquadrar decisões e estratégia de negócios. Um dia, vou escrever um livro de negócios realmente chato com um capítulo para cada um, mas até então você terá que se contentar com este blog, que cobre o que eu acho que é o mais útil.

This key question is, “Given the current state of the market, are there any future outcomes that are likely to occur in almost any future state?” Or, in short, “Are there any inevitabilities?”

It’s rarely possible to predict specific events or exactly when things might happen,but it’s been surprisingly easy to spot larger trends that are sure to happen over a long time horizon. It’s served me well as I’ve bet on the unavoidable rise in the value of clean energy and the O custo imparável diminui causado pelo aprendizado de curvas em tecnologias limpas. Ambas foram tendências bastante óbvias a partir de meados dos anos 2000 e hoje estão subjacentes ao sucesso de empresas multibilionárias e algumas das indústrias que mais cresce na Terra. terá sido feito nesse ponto. Estou simplesmente apontando que as mudanças climáticas não para 1,5 graus. Ele continua, com consequências cada vez mais cataclísmicas, de modo que mesmo os defensores mais teimosamente ignorantes do status quo acabarão implorando por alternativas de carbono zero.

A global response to climate change is inevitable, and the resulting economic changes are fairly obvious if you look closely enough. I am not going to attempt to guess when the planet will respond, nor to speculate on how much irreversible damage will have been done by that point. I am simply pointing out that climate change doesn’t stop at 1.5 degrees. It keeps going, with ever more cataclysmic consequences such that even the most stubbornly ignorant defenders of the status quo will eventually be begging for zero carbon alternatives.

This conjecture leads to some pretty simple conclusions about our future state.

- O carbono acabará tendo um preço.

- Somente soluções multi-gigaton realmente importantes. Solução.

- Value will be increasingly concentrated in the green attributes of certain products, not the products themselves.

- Negative emissions technologies will be required.

- Retrofitting and reuse of current infrastructure must be a large part of the solution.

- A adaptação em larga escala é inevitável. Por enquanto, estou focado no que podemos intuir sobre a economia nesse estado futuro, porque definir uma estratégia de negócios é muito mais fácil quando você conhece o futuro, ou pelo menos uma aproximação aproximada dela. No estado futuro, definimos acima,

There’s a lot to unpack in each of these. For now I’m focused on what we can intuit about the economy in this future state, because defining a business strategy is far easier when you know the future, or at least a rough approximation of it. In the future state we have defined above, É provável que vejamos o surgimento de vários trilhões de dólares que simplesmente não existem hoje. Cargas I call these the Five Inevitable Industries and they are listed below.

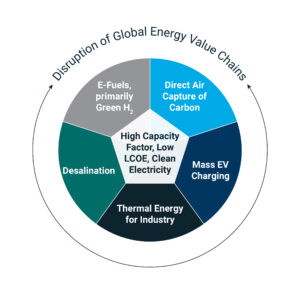

- Green Hydrogen and E-Fuels

- Direct Air Capture

- Electrification of Industrial Thermal Loads

- CARREGA DE MASS EV

- Desalinização e transporte de água

Pode ser que apenas um casal chegue a escalar ou que outros emergem que não estão nesta lista. Mas acho que contar com o surgimento dessas cinco indústrias é uma boa aposta em relação a outros prognósticos que você poderia fazer sobre o nosso futuro de carbono zero.

Por que esses são esses? E o que os torna inevitáveis é: Because these are based primarily on what MUST happen, what is inevitable. And what makes them inevitable is:

- Eles são massivamente escaláveis, beneficiando -se das economias de escala, tanto dentro de sua cadeia de suprimentos quanto também dentro de cada instalação. Solar. Existem melhores soluções?

- They leverage existing technologies relying only on the well understood learning curves that come with mass deployment.

- They benefit from the rapid improvement of adjacent technologies, such as wind and solar.

- The entrenched political and business interests are least threatened by and likely to see the most opportunity for themselves in these new industries.

- These industries have the ability to reuse or retrofit large portions of today’s industrial and energy infrastructure with dramatically reduced carbon emissions.

- Together they are sufficient to all but solve our climate problem.

Are there better solutions? Depende de quem você pergunta. Existem muitos outros valores pelos quais você pode medir nossa resposta às mudanças climáticas e, por extensão, julgar essas soluções. Quando digo que são inevitáveis, é baseado no que vejo como o conjunto atual de fatos no solo e no valor singular de parar as emissões antes que seja tarde demais. consumindo. Não me interpretem mal, ainda sou um cara de todos os altos e algumas dessas alternativas são coisas que eu gostaria que acontecesse com base em meus próprios valores, mas se você estiver prevendo as indústrias de trilhões de dólares de amanhã, não serão eles. Mais sobre isso na próxima parcela. Primeiro, cada um atualmente é tecnologias disponíveis que estão sendo tornadas econômicas pela crescente abundância de fatores de alta capacidade, eletricidade limpa e de baixo custo. O extraordinário

None of these will satisfy the type of values-based advocacy or narrow efficiency arguments that lead you down the road of rooftop solar, the unlikely permitting of a massive number of new nukes, catching cow farts, or simply demanding that everyone stop driving and consuming. Don’t get me wrong, I’m still an all-of-the-above guy and some of these alternatives are things I wish would happen based on my own values, but if you’re predicting the trillion dollar industries of tomorrow, these will not be them.

Perhaps the most telling predictor of these Five Inevitable Industries is what they have in common. More on that in the next installment.

PART TWO: High Capacity Factor, Low Cost, Clean Electricity is The Nexus Of Deep Decarbonization

So what do all of the Five Inevitable Industries have in common? First, they are each currently available technologies that are being made cost effective by the increasing abundance of high capacity factor, low-cost, clean electricity. The extraordinary O custo diminui em eletricidade renovável nos permite aproveitar o setor em que fizemos o maior progresso nas últimas duas décadas para descarbonizar o restante de nossa sociedade. essas indústrias. Embora todas essas tendências sejam impulsionadas pelo fato de que o carbono terá preços diretamente (ou indiretamente através de créditos tributários, etc.) e as soluções multi-gigaton serão priorizadas, o hidrogênio verde e os combustíveis eletrônicos são ainda mais direcionados pela necessidade de retrofit e reutilização da infraestrutura atual. Se esperarmos por todos os motores de avião, turbinas a gás, caldeiras industriais, siderúrgicas, navios e outras infraestruturas existentes a serem substituídas, será tarde demais.

High Capacity Factor, Low LCOE, Clean Electricity in the Nexus of Deep Decarbonization

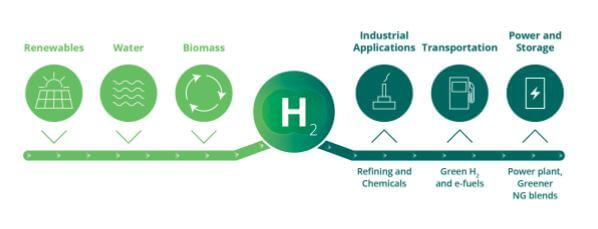

Green Hydrogen and E-fuels are perhaps the most advanced, or at least the most talked about, of these industries. While all of these trends are driven by the fact that carbon will be priced either directly (or indirectly through tax credits, etc) and multi-gigaton solutions will be prioritized, Green Hydrogen and E-fuels are further driven by the need for the retrofit and reuse of current infrastructure.

Green Hydrogen and E-fuels are perhaps the most advanced, or at least the most talked about, of these industries. While all of these trends are driven by the fact that carbon will be priced either directly (or indirectly through tax credits, etc) and multi-gigaton solutions will be prioritized, Green Hydrogen and E-fuels are further driven by the need for the retrofit and reuse of current infrastructure.

The capital expenditure and time required to replace all carbon intensive infrastructure in the necessary time frame is prohibitive. If we wait for all airplane engines, gas turbines, industrial boilers, steel mills, ships and other existing infrastructure to be replaced, it will be too late. A infraestrutura é persistente, especialmente infraestrutura amplamente distribuída, como motores de avião que são fontes pontuais individualmente, mas compõem uma fonte enorme de emissões coletivamente. Eles são muito mais difíceis de trocar do que as usinas de energia da escala de utilidade, que são fontes muito mais centralizadas de emissões de carbono. Os argumentos sobre coisas como "bem a eficiência de roda" do hidrogênio verde cairão, pois fica claro que a energia de entrada é barata o suficiente, e o prêmio de flexibilidade de combustíveis líquidos e gasosos em determinadas aplicações é alta o suficiente, para tornar a eficiência geral menos relevante. Veremos isso em aplicações como a aviação, mas também em certos setores, como a fabricação de aço e cimento que requerem combustíveis capazes de produzir calor e vapor com uma qualidade que a eletrificação não pode atender no curto prazo.

Moreover, liquid and gaseous fuels have an energy density, storage properties and other flexibility that make them far more valuable than electrons on a wire. Arguments about things like “well to wheel efficiency” of green hydrogen will fall away as it becomes clear that input energy is cheap enough, and the flexibility premium of liquid and gaseous fuels in certain applications is high enough, to make overall efficiency less relevant. We’ll see this in applications such as aviation, but also in certain industries such as the manufacture of steel and cement that require fuels capable of producing heat and steam at a quality that electrification cannot meet in the near term.

Simplificando, a transição exigirá zero combustíveis de carbono que sejam substituições "que caem" para hidrocarbonetos. As soluções de emissões negativas serão necessárias. São necessárias grandes quantidades de energia para alimentar os processos químicos que capturam e sequestram carbono da atmosfera. Felizmente, temos uma quantidade crescente de fator de alta capacidade, eletricidade limpa e de baixo custo para alimentar esses processos, e isso está permitindo que os primeiros projetos em larga escala se tornem viáveis. À medida que esses projetos são construídos e descemos a curva de aprendizado na tecnologia direta de captura do ar, o custo dessas instalações cairá, permitindo que elas funcionem com energia que pode ter um fator de menor capacidade ou ser um pouco mais caro. Isso aumentará a pegada geográfica sobre a qual essas tecnologias podem competir da mesma maneira que as renováveis foram feitas nas últimas duas décadas. É importante observar que

But net zero will not be achievable in all sectors and even if it is, by that point net zero will no longer be enough. Negative emissions solutions will be required.

Today’s direct air capture technologies are “too expensive” partly due to their energy intensity. It takes massive amounts of energy to fuel the chemical processes that capture and sequester carbon from the atmosphere. Luckily, we have an increasing amount of high capacity factor, low-cost, clean electricity to fuel such processes, and this is enabling the first large scale projects to become feasible. As these projects are built and we come down the learning curve on direct air capture technology, the cost of these facilities will fall, allowing them to run on energy that may have a lower capacity factor or be slightly more expensive. This will increase the geographic footprint over which these technologies can compete in much the same way that renewables have done in the past two decades. It’s important to note that Este ciclo virtuoso de custos decrescentes, permitindo fatores de menor capacidade ou insumos de energia limpa mais caros, é uma característica de quase todas as nossas cinco indústrias inevitáveis. Por exemplo, se você pode tirar o carbono da atmosfera por US $ 200/tonelada, uma solução para impedir que o carbono seja colocado na atmosfera precisará ser inferior a US $ 200/tonelada para fazer sentido. Mesmo que uma tecnologia seja um pouco mais cara do que esse preço de "traseiro", os limites do armazenamento subterrâneo e hesitação dos ambientalistas em aceitar sequestro como uma solução permanente provavelmente impedirão a captura direta do ar de deslocar outros esforços para descarbonizar a economia. Em vez disso, nos permitirá mais tempo para avançar o hidrogênio verde, a limpeza de aço e outras soluções de carbono zero e potencialmente fornecer um mecanismo para desfazer alguns dos danos que já fizeram. Isso é uma simplificação excessiva, mas não muito longe da marca.

Direct air capture will likely be the “backstop” technology for carbon abatement against which most other solutions are measured. For instance, if you can take carbon out of the atmosphere for $200/ton, a solution to stop carbon from being put into the atmosphere will need to be less than $200/ton to make sense. Even if a technology is slightly more expensive than this “backstop” price, the limits of underground storage and hesitancy of environmentalists to accept sequestration as a permanent solution will likely keep direct air capture from displacing other efforts to decarbonize the economy. Instead it will allow us more time to advance green hydrogen, clean steel and other zero carbon solutions and potentially provide a mechanism to undo some of the damage that we have already done.

Currently, 30% of all carbon emissions come from industrial loads, 2/3 of which are produced from boiling water. That’s a gross oversimplification, but not too far off the mark. Nossa economia consome enormes quantidades de vapor para vários processos industriais. Grande parte desse vapor é produzida em caldeiras ou cogeração de algum tipo usando combustíveis fósseis, principalmente gás natural. Quando a maioria das pessoas pensa em "eletrificação", pensa em cidades como Berkeley, CA, rasgando o sistema de distribuição de gás e exigindo que todos usem um fogão de indução, mas essa abordagem e a controvérsia de alto perfil que o envolvem são a energia solar na cobertura da eletrificação térmica. Em outras palavras, altamente visíveis, distribuídos desiguais e objeto de um debate infinito, mas, finalmente, não é de escala suficiente para ser importante ao longo do horizonte de tempo em que a agulha é encontrar maneiras de eletrificar a produção da produção de vapor ou a panificação, a seca, a fusão e os processos de calor direto encontrados em grandes instalações industriais. Grandes partes desse trabalho precisarão ser feitas com caldeiras elétricas alimentadas com fator de baixo custo e alta capacidade, eletricidade limpa ou usando hidrogênio verde e combustíveis eletrônicos feitos com a mesma entrada. As caldeiras elétricas e tecnologias semelhantes já podem fornecer vapor a pressões e temperaturas adequadas para lidar com grandes partes desse mercado. O refrão típico de soluções elétricas que não é capaz de atender às necessidades de qualidade desse mercado é limitado a algumas aplicações específicas, deixando uma grande maioria desse mercado aberto à eletrificação. De fato, mesmo essas aplicações de alta temperatura podem ser eletrificadas substituindo o hidrogênio verde ou outros combustíveis feitos de eletricidade limpa pelos combustíveis fósseis atualmente em uso.

What will truly move the needle is finding ways to electrify the production of steam or the baking, drying, melting and similar direct heating processes found in large industrial facilities. If the decarbonization of these loads is inevitable it is almost certain that large portions of that work will need to be done with either electric boilers powered with low cost, high capacity factor, clean electricity or using green hydrogen and e-fuels made from that same input.

Technologies that exist today can likely address much of this market for clean industrial thermal loads. Electric boilers and similar technologies can already provide steam at adequate pressures and temperatures to address large portions of this market. The typical refrain of electric solutions not being able to meet the quality needs of this market is limited to a few specific applications, leaving a huge majority of this market open to electrification. In fact, even those high temperature applications can be electrified by substituting green hydrogen or other fuels made from clean electricity for the fossil fuels currently in use.

This market in particular will require high capacity factor electricity or efficient storage of thermal energy as many steam loads are continuous and interruptions will be costly to the industrial processes that they support. Este é um tema recorrente ao longo das cinco indústrias inevitáveis e por que sou tão pedante em me referir não apenas à energia limpa, mas a baixo custo, fator de alta capacidade, eletricidade limpa.

Parte três: quem faz a bomba de gás? Quem faz a gasolina? De qual você já ouviu falar? Essas indústrias mal existem hoje, diferentemente dos veículos elétricos que muitos acreditam que já estão a caminho da adoção em massa. Mas o EV cobrando como sabemos que está em sua infância. À medida que avançamos em direção ao carregamento agregado ou em massa de EV, como às vezes me referi a ele, passamos além das agradáveis interfaces e carregadores de software que se parecem com bombas de gás.

So far we’ve hit on three of the Five Inevitable Industries – Green Hydrogen and E-fuels, Direct Air Capture and Thermal Electrification. These industries barely exist today, unlike electric vehicles which many believe are already on their way to mass adoption. But EV charging as we know it is in its infancy. As we move toward aggregated or mass EV charging as I’ve sometimes referred to it, we move beyond pleasant software interfaces and chargers that look like gas pumps. Vamos precisar de atualizações da grade de distribuição para passar de 5 a 10 carregadores no canto de um estacionamento para eletrificar uma porcentagem significativa de toda a garagem. Os ativos com uso intensivo de capital precisarão ser implantados com uma combinação de especialização em mercados de energia elétrica, imóveis, finanças e por atacado. As cargas de carregamento agregadas participarão cada vez mais de mercados de energia no atacado como cargas e ativos de armazenamento. Bilhões de dólares em ativos de armazenamento no nível de distribuição precisarão ser implantados, financiados e otimizados para amortecer cada local de carregamento em massa. Gigawatt Horas de fator de alta capacidade, baixo custo e eletricidade limpa precisará ser adquirida para atender a uma curva de carga em constante mudança. Essa compra será feita em mercados de energia que também estão passando por uma volatilidade e mudança maciças à medida que aceitam geração mais renovável, ativos de armazenamento e choques da eletrificação de outros setores. A resposta óbvia aqui são as empresas de rede de cobrança, recém -saídas de seus respectivos espaçamentos e investindo como loucos em suas próprias redes. Mas cavar um pouco mais fundo e pergunte a si mesmo se as funções acima - financiamento de ativos, desenvolvimento e gerenciamento de demanda maciça e dinâmica por energia limpa - são competências essenciais para qualquer uma dessas empresas. Por um longo tempo, eu assumi que os utilitários dominariam esse espaço com investimentos em infraestrutura de nível de distribuição, armazenamento de borda de grade em larga escala, tarifas de carregamento e similares. No entanto, a velocidade com que os utilitários estão se movendo não me dá confiança de que eles chegarão lá a tempo. Isso deixa um mercado maciço sem um vencedor claro. When this change occurs, EV charging is at least as much about the deployment of massive utility scale infrastructure as it is about charging networks, member growth, network effects and software.

Highly capital-intensive assets will need to be deployed with a combination of expertise in electric power, real estate, finance and wholesale power markets. Aggregated charging loads will increasingly participate in wholesale power markets as both loads and storage assets. Billions of dollars worth of distribution-level storage assets will need to be deployed, financed and optimized to buffer each mass charging site. Gigawatt hours of high capacity factor, low cost, clean electricity will need to be procured to meet a constantly shifting load curve. This procurement will be done in power markets that are also undergoing massive volatility and change as they accept more renewable generation, storage assets and demand shocks from electrification of other sectors.

In short, a trillion dollar market with a capital intensive and complex upstream supply chain must manifest where until just recently there was nothing.

The big question within this Inevitable Industry is who will win. The obvious answer here is the charging network companies, fresh off their respective SPACs and investing like crazy in their own networks. But dig a little deeper and ask yourself whether the functions above – asset finance, development and managing massive and dynamic demand for clean energy — are core competencies for any of these companies.

It is far more likely that the charging networks will expand by bundling services and other innovative marketing focused on network growth than by vertically integrating back upstream into hard infrastructure. For a long time, I had assumed that the utilities would dominate this space with investments in distribution level infrastructure, large scale grid edge storage, charging tariffs and the like. However, the speed with which the utilities are moving does not give me confidence that they will get there in time. This leaves a massive market without a clear winner.

The scale of energy demand and delivery that will eventually result from these massive charging networks will be like nothing the grid has ever seen. Com cumprimento da promessa da revolução EV, é pelo menos tanto sobre a construção, financiamento, gerenciamento e despacho de ativos de infraestrutura em escala de utilidade quanto sobre os próprios carros. estar idealmente situado para capturar valor no eventual mercado de carregamento de trilhões de dólares das próximas décadas. A indústria inevitável final que vejo emergente é um pouco diferente, pois não é uma solução focada na redução de emissões, mas uma adaptação inevitável que nossa sociedade será forçada a fazer. As tecnologias de dessalinização e transporte transformam o problema da água em um problema de energia. Isso não resolve necessariamente o problema da água, mas em um mundo cada vez mais insignificante em abundante eletricidade limpa, nos dá um caminho para converter o This is why I believe that the inevitable switch to EVs and the associated need for aggregated EV charging depends on the generation and delivery of massive amounts of high capacity factor, low cost electricity, and those with expertise in this area will be ideally situated to capture value in the eventual trillion dollar EV charging market of the next few decades.

PART FOUR: The Future of Water Is Clean Energy

So far we’ve focused on the rise of technologies that will solve the climate crisis and eliminate our emissions problem. The final Inevitable Industry that I see emerging is a little different in that it is not a solution focused on emissions reduction, but rather an inevitable adaptation that our society will be forced to make.

Access to clean, fresh water will be one of the largest challenges of climate change. Large portions of the world will lose reliable access to water for purposes of drinking, irrigation, sanitation and industry. Desalination and transportation technologies turn the water problem into an energy problem. That doesn’t necessarily solve the water problem, but in a world increasingly awash in abundant clean electricity, it gives us a pathway to convert the 97% da água na Terra que não é potável em água potável e utilizável e mova -a para onde é mais necessário. Isso se encaixa no perfil exato das outras indústrias inevitáveis, permitindo que a dessalinização seja possibilitada pela primeira vez por eletricidade limpa e de baixo custo e de alto custo. Eventualmente, uma vez que o custo diminuiu com a implantação em massa de equipamentos de dessalinização, ampliando a pegada onde a dessalinização pode ser econômica para áreas onde o fator de alta capacidade, a eletricidade limpa pode ser um pouco mais cara. E um volume tão grande, o transporte de longa distância só aumentará à medida que o mundo busca distribuir água dessalinizada ou águas superficiais de lugares que permanecem molhados a lugares que estão vendo suprimentos de água diminuindo. Para uma economia de baixo carbono, há uma questão em aberto em relação a todas essas indústrias inevitáveis que eu acho que vale a pena abordar. A localização dessas cinco indústrias inevitáveis vai para o coração de como elas se desenvolverão e quem se beneficiará dessa revolução industrial verde. Veremos as renováveis de "escala industrial" nos bastidores com custos nivelados menos favoráveis da eletricidade mais próximos dos centros industriais existentes, pagando um pouco mais por energia limpa, mas evitando os custos da entrega da grade? Ou veremos realmente o realinhamento de toda a economia industrial, com muitas dessas novas cargas limpas optando por localizar em áreas onde elas podem acessar renováveis nos bastidores ou de outra forma mais baratos, com energia limpa entregue à grade?

Desalination is a proven technology but it is highly energy intensive and still has a relatively high capital cost. This fits the exact profile of the other Inevitable Industries, allowing desalination to at first be enabled by broadly available low cost, high capacity factor, clean electricity. Eventually, once the cost has declined with mass deployment of desalination equipment, broadening the footprint where desalination can be economical to areas where high capacity factor, clean electricity may be a little more costly.

Water transportation doesn’t exhibit quite the same dynamic, but it is worth mentioning as water pumping loads already consume massive amounts of electricity in places like the American West where water is moved in large volumes for use in agriculture. And such large volume, long distance transport will only increase as the world seeks to distribute desalinated water or surface water from places that remain wet to places that are seeing decreasing water supplies.

PART FIVE: Industrial Scale Behind-The-Meter and The Remaking Of Retail Energy

As I wrap up this five part series on the Nexus of Deep Decarbonization and Intersect Power’s vision for a low carbon economy there is one open question with regard to all of these Inevitable Industries that I think is worth addressing. The location of these Five Inevitable Industries goes to the heart of how they will develop and who will benefit from this green industrial revolution.

Will we see electricity, green hydrogen or other energy carriers delivered over existing infrastructure to current industrial centers where these new industries will take root? Will we see “industrial scale” behind-the-meter renewables with less favorable levelized costs of electricity closer-in to existing industrial centers, thereby paying a little more for clean energy but avoiding the costs of grid delivery? Or will we actually see the realignment of the entire industrial economy with many of these new clean loads choosing to site in areas where they can access behind-the-meter renewables or otherwise cheaper grid-delivered clean energy?

acho que será uma combinação de todas essas três coisas. Mas uma coisa é clara, pois uma parte significativa de nossa economia existente e emergente requer eletrificação, será uma bola de salto entre a infraestrutura de gás, que atualmente serve grande parte dessa carga, infraestrutura de eletricidade e alternativas para o final do meio do metro para ver quem pode oferecer soluções mais econômicas para essa mudança de energia industrial. Mesmo aumente as estruturas regulatórias nos mercados de hoje.

The outcome of this free-for-all will dictate which entities own the customer relationships across the energy industry and might even upend the regulatory structures in today’s markets. Este é o elemento final das cinco indústrias inevitáveis-interrupção maciça do modelo de negócios de energia de utilidade e varejo. If low cost, high capacity factor, clean electricity is the nexus which links and enables the Five Inevitable Industries, then the disruption of today’s midstream and downstream business models is the consequence of the realignment in energy demand that will come about as these Inevitable Industries scale. This is not what I think of as one of the Inevitable Industries per se, but more of a knock-on effect of these Inevitable Industries. If low cost, high capacity factor, clean electricity is the nexus which links and enables the Five Inevitable Industries, then the disruption of today’s midstream and downstream business models is the consequence of the realignment in energy demand that will come about as these Inevitable Industries scale.

By now you’re tired of hearing it, but all of the above can be simplified down to the following: High capacity factor, low cost, clean electricity is the Nexus de descarbonização profunda. Ele permitirá que eles implantem em escala e desça a curva de custo para seu próprio Capex, permitindo que eles comprem mais eletricidade limpa e provavelmente reduzindo ainda mais o custo dessa eletricidade, trazendo ainda mais a sua própria curva de aprendizado. Este

It is the enabling factor that “turns on” these new zero carbon, trillion dollar industries. It will enable them to deploy at scale and come down the cost curve for their own capex, enabling them to buy more clean electricity and likely reducing the cost of that electricity further by bringing renewable generation technologies even further down their own learning curve. This Ciclo virtuoso de demanda e escala é a maior esperança que temos para resolver a crise climática. Essas coisas nos dividem hoje ainda mais do que na história humana recente. Mas, como seres humanos, também nos distinguimos por nosso instinto de sobrevivência, nossa capacidade de inovação e nossa compaixão por outras pessoas que sofrem. Eu escolho acreditar que serão essas três últimas características que finalmente definem nossa resposta às mudanças climáticas. Por causa disso, não consigo imaginar um futuro em que não conseguimos abordar essa crise. Se meu otimismo estiver correto, há muitas razões para acreditar que uma grande parte do exposto é, de fato, inevitável.

As a species, we are susceptible to a whole host of inconvenient traits including selfishness, mass delusions and the emotional desire to feel like an important part of an accepted group or something greater than ourselves. These things divide us today even more so than they have in recent human history. But as humans, we are also distinguished by our survival instinct, our capacity for innovation and our compassion for others who suffer. I choose to believe that it will be these last three traits that ultimately define our response to climate change. Because of this I cannot imagine a future where we fail to address this crisis. If my optimism is correct, then there is ample reason to believe that a large portion of the foregoing is, in fact, inevitable.